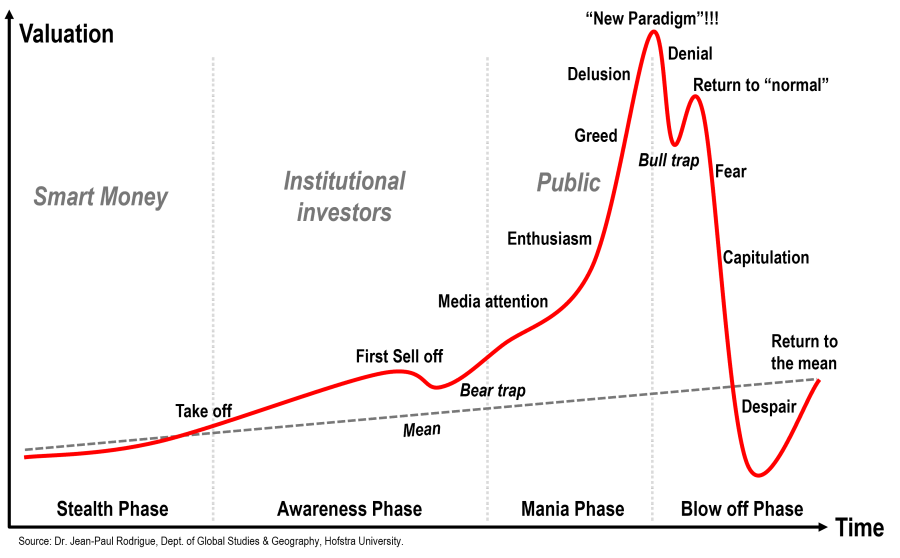

Are we in an AI bubble?

Yes. But that does not mean the technology is fake, or that the opportunity is over.

The short answer is yes.

We are in an AI bubble.

But that answer is too short, and honestly, it removes the interesting part. A bubble is not always a sign that the underlying technology is fake. Sometimes it is just what happens when a real platform shift meets too much capital, too much narrative, and too many people trying to front-run the future.

That is how I see AI right now.

There is real technology here. Even if multimodal models stopped improving today, there is already a ridiculous amount of value that companies have not captured yet.

The problem is that the financial cycle around the technology can still get ahead of the value that has actually been deployed.

Both things can be true at the same time.

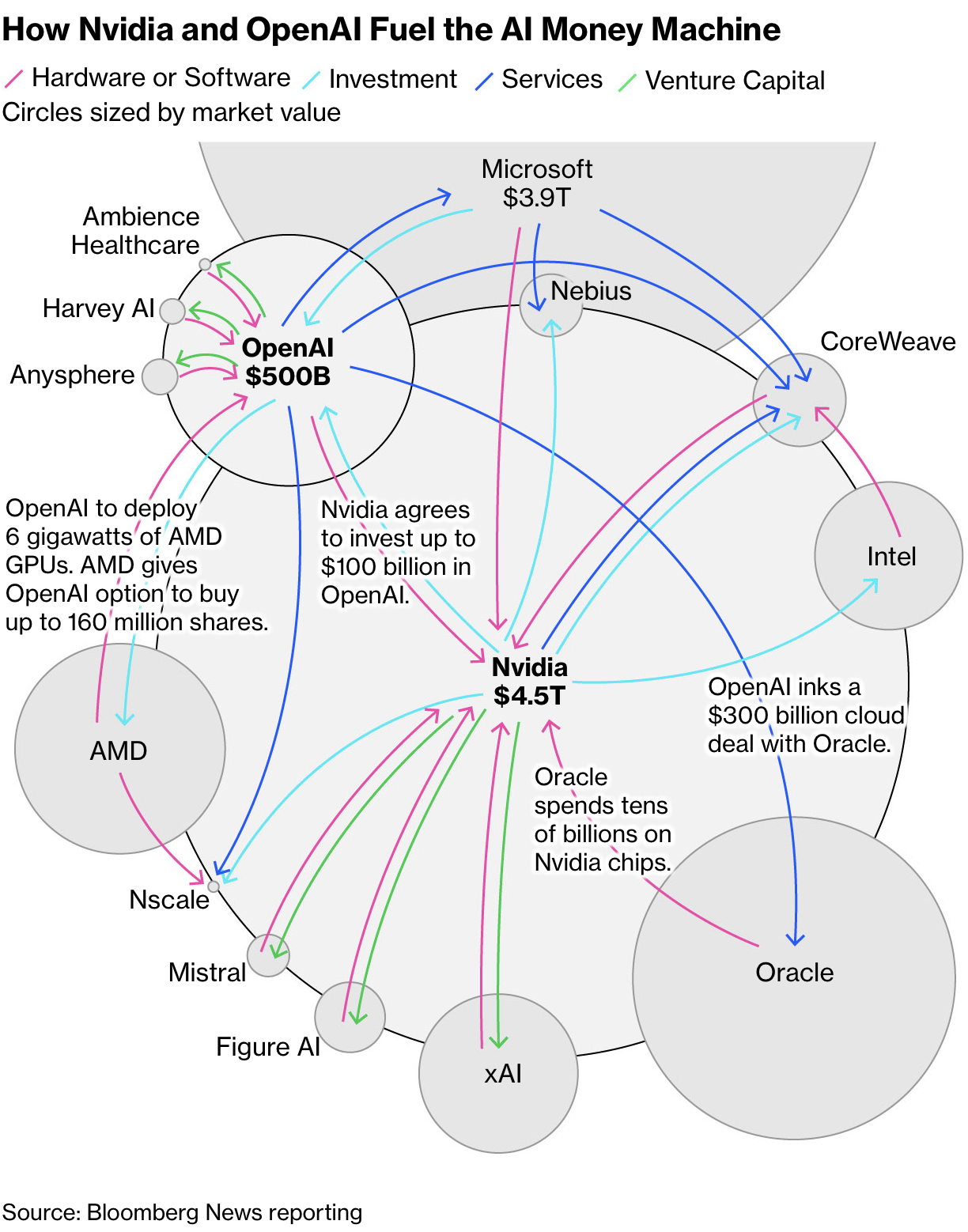

The circular deals

For months, there has been a strange pattern in some of the biggest AI deals.

A lab needs compute. A cloud provider needs revenue growth. So the cloud provider invests a huge amount of money in the AI lab, and then the AI lab commits to spending most of that money back on compute from the same provider.

On paper, everyone wins.

- The cloud provider reports a massive customer contract.

- The AI lab raises at a higher valuation.

- Existing investors get more paper gains and more liquidity options.

- The story keeps moving.

This does not mean the deal is fake. The lab really does need compute. The cloud provider really does sell infrastructure. There is a rational business logic underneath it.

But the loop matters.

That compute is usually paying for two things:

- Training new models.

- Running inference, which is what users feel every time they ask a model to do something.

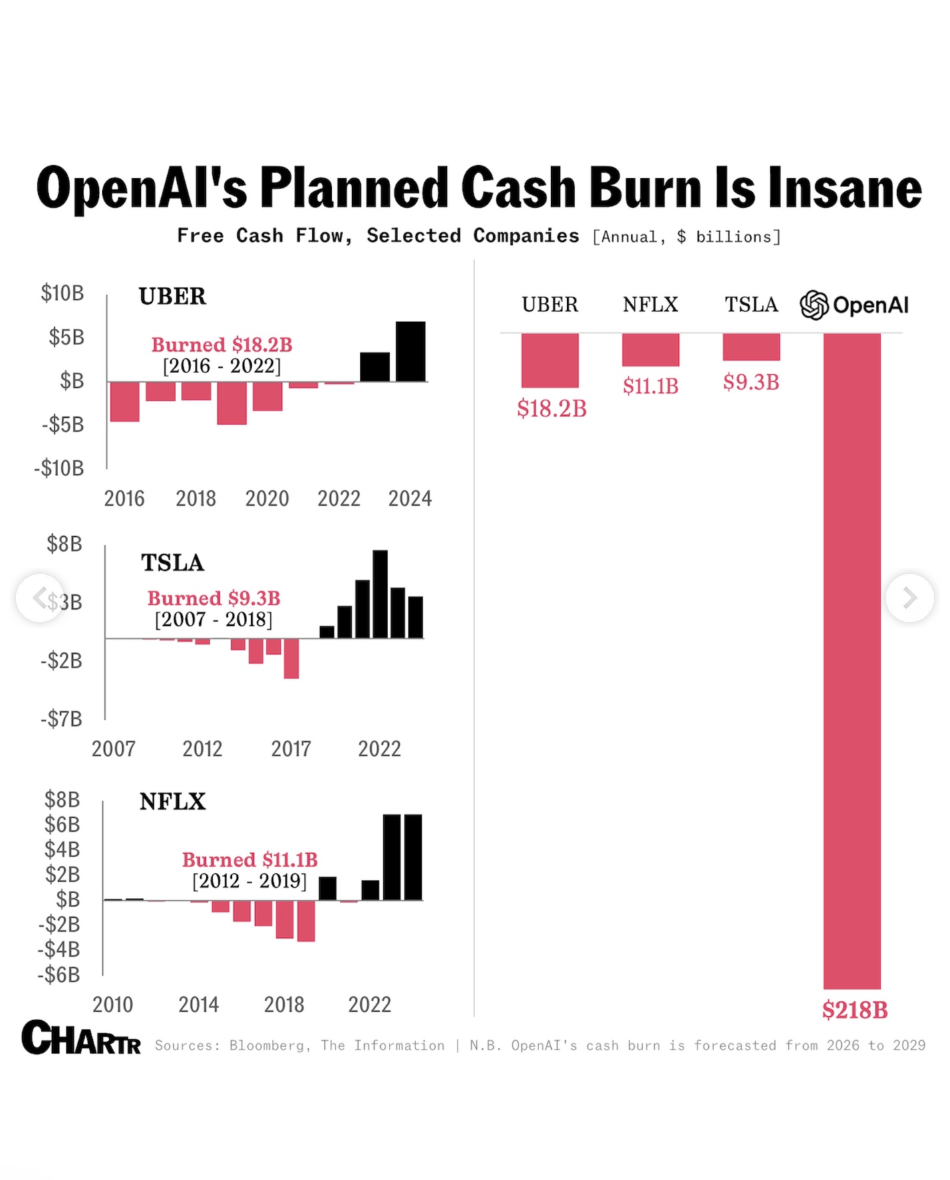

Because a large part of the current AI economy is not yet profitable. A lot of usage is being subsidized so companies can acquire users, grow revenue, and defend the narrative that the market is still early enough to justify massive valuations.

Every ChatGPT, Claude, Gemini, or Grok response has a compute cost. Today, many of those costs are still being absorbed by companies that are prioritizing growth over profitability.

That can work for a while.

It cannot work forever.

There is also a bigger question, which Dario Amodei discussed publicly: how profitable is a frontier model when the next model is already being trained by the time the current one reaches users?

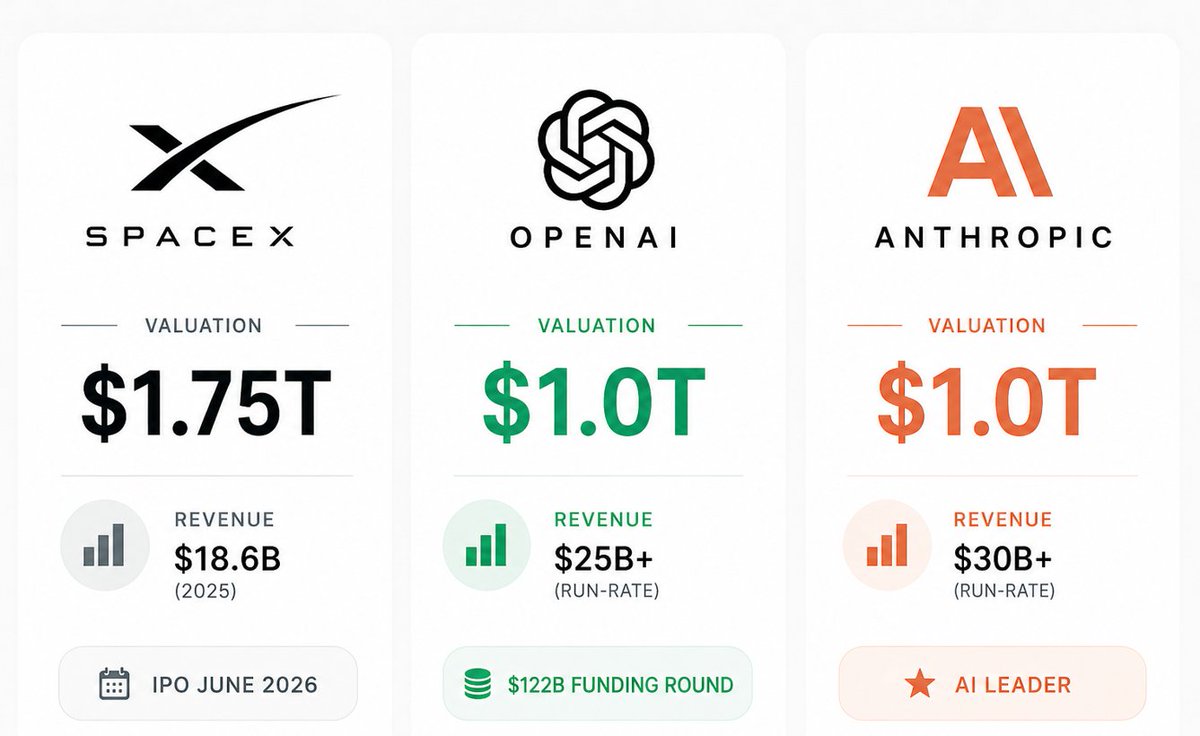

The IPO problem

Private companies usually have two big liquidity paths:

- They get acquired.

- They go public.

For companies like OpenAI, Anthropic, or SpaceX-sized private companies, a traditional acquisition becomes almost impossible because very few buyers can acquire something at that scale.

So the real path is the public markets.

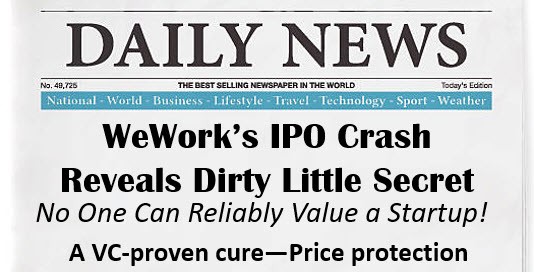

The problem is that going public forces companies to show reality. An S-1 does not care about vibes. It shows revenue, losses, margins, risk, dependencies, and the actual shape of the business.

This is where the comparison to WeWork matters. WeWork had an incredible narrative until the public markets saw the financials and decided the story did not support the valuation.

AI is different from real estate. I do not want to make a lazy comparison.

But there is one uncomfortable similarity: many of these companies burn money extremely fast and are not close to being profitable.

The only way that does not scare public markets is if revenue is growing so fast that investors accept the burn.

Maybe that happens.

But we should be honest about the tension: some of that growth is also powered by cheap or subsidized compute.

What happens when the music slows down?

At some point, it will become harder to keep subsidizing model usage at the current level.

We already see hints of this. Some products restrict usage. Some models get more expensive. Some companies change plans, reduce token limits, or push users into higher tiers.

Anthropic has already had to increase Claude usage limits through a compute deal with SpaceX.

The point is simple: a cheap subscription can look cheap only because someone else is absorbing part of the real compute cost.

And if inference prices go up, behavior changes.

Today I use AI for things that would feel irrational if I had to pay the true cost every time. I might ask a coding agent to change a button color or replace an image because it feels cheap and abundant.

But if model usage becomes much more expensive, we will stop using LLMs for everything.

That has consequences.

The first one is that many thin AI wrappers will struggle. If your product depends entirely on a third-party model and the cost structure changes, your business can break overnight.

That is why some companies are trying to own more of the model layer. It is not only technical ambition. It is survival.

The second consequence is that investment into "AI companies" will cool down.

When bubbles pop, people do not calmly separate the good companies from the bad ones on day one. They panic. Capital gets more conservative. Hiring slows down. Startups die, including some that probably had real technology.

I would not be surprised if, after the correction, the number of AI startups falls sharply for a few years.

That sounds negative.

But I do not think it means people should stop adopting AI.

Actually, I think the opposite.

The opportunity is still real

The dot-com bubble killed a huge number of companies. It also gave us Amazon, MercadoLibre, Netflix, Facebook, and many other companies that used the internet as real infrastructure.

I think AI will rhyme with that.

Many companies will die. But the companies that already have customers, real workflows, and operational pain can use AI to redesign services, operations, and processes in a very concrete way.

That is the part I care about.

The technology already works well enough to create value in many boring, high-friction workflows.

I still find it crazy that I can build a decent website in days when, a few years ago, the same thing would have taken much longer. I can improve design work with image models. I can analyze hundreds of transcribed calls in ways that would have been painful before.

That is not hype.

That is leverage.

Why Latin America is interesting

Latin America is full of service businesses: legal, accounting, logistics, healthcare, back office, call centers, construction, industrial services, and a long list of B2B operations.

In many of these categories, the client does not really care how the work gets done.

They care about the outcome.

That creates a real opportunity to turn traditional service companies into AI-native service companies.

Examples are easy to imagine:

- In radiology, AI can read images, patient history, and generate a draft report that a radiologist reviews and approves.

- In accounting, agents can help with reconciliations, invoices, accounts receivable, accounts payable, audits, and reporting.

- In legal work, AI can review contracts, extract risks, prepare responses, and summarize case documentation.

- In manufacturing, computer vision can support quality control, predictive maintenance, procurement analysis, and production planning.

- In construction and real estate, teams can automate proposals, budgets, schedules, reports, contract review, and change tracking.

The human does not disappear.

The human moves toward judgment, validation, strategy, and accountability.

My current view

Yes, we are in a bubble.

But no, I do not think the conclusion is "AI is fake."

The better conclusion is:

The financial cycle can break, while the technology keeps compounding.

That means many companies built only on narrative will disappear. But companies with real customers, real operations, and the willingness to redesign how work gets done can come out stronger.

The opportunity is not to add AI on top of broken processes.

The opportunity is to rebuild the process around what the technology now makes possible.